If you cannot see the graphic or access the links within this message please go to the source

|

|

Positive signals from occupiers trumped by external noise

For those with the inclination to look for them, there have been plenty of encouraging signs from occupiers in recent months. In the much-maligned office sector, Central London delivered a strong finish to 2024, including a record rent for the City at 22 Bishopsgate. The same office building, the City’s largest, then let its last available space in January. Amex have agreed to upsize by two thirds in Victoria, whilst Jane Street Capital are reported to be looking to double the space they currently occupy, with a requirement of up to half a million square feet.

In Manchester, Bruntwood SciTech have signed up Autotrader amongst others to No3 Circe Square, taking the scheme to almost 70% let during construction. The same developer also agreed a 50,000 sq ft letting at their new life sciences scheme in Birmingham.

In the long-suffering shopping centre sector, Australian homewares retailer Harvey Norman agreed a 20-year lease on 53,000 sq ft of space in Sutton Coldfield which has lain vacant since the failure of BHS in 2016. New River REIT reported that it had reached 96% occupancy, despite absorbing the Capital & Regional portfolio last year, with their recent lettings included a former Homebase being taken by Sainsbury’s at a rent 60% ahead of ERV.

|

Elsewhere, Tesco paid £63m at a sub 5% yield to buy back their own store in Newmarket. In Manchester, Nobu have committed to opening their first UK restaurant outside London, alongside a hotel and 452 apartments.

However, these individually small but cumulatively significant news stories have been all but drowned out by geopolitics, and as a result most investors continue to sit on their hands. The investment market has had a very slow start to the year, even by the moribund standards of recent years.

In February, none of the traditional commercial sectors delivered anything of real substance, whilst even the hereto resilient residential sectors went quiet against the backdrop of volatile bond yields. Rarely can there have been such disparity between encouraging occupier trends and cloying hesitancy in the investment market. |

|

Commercial property returns

According to MSCI, average commercial property values edged upwards by 0.1% in February, taking the cumulative recovery to 2.2% since last April. Nonetheless, average values are still 23.4% below their June ’22 peak, despite rental values increasing by 9.8% over the same period.

Retail Parks have been the strongest performing sub-sector over the last 12 months, with capital growth of 6.6%. After many years of decline Shopping centre values have edged higher year-on-year (2.2%), as have supermarkets (1.3%). Shop values are still down 2.5% year-on-year but have shown possible signs of stabilisation in recent months.

The recovery in Industrial values picked up pace towards the back end of 2024, and annual growth reached 4.6% in February. Rental growth has been robust (5.5% year-on-year), albeit it has slowed steadily since reaching double-digit growth rates in 2021/22.

Capital values in the office sector are down by 3.9% year-on-year on average, but the rate of decline has moderated quite materially. Six months ago, office values were declining at an annul rate of 11.7%. In the most recent six-month period, office values in parts of the South East (driven by Life sciences), and the West End of London have edged upwards. |

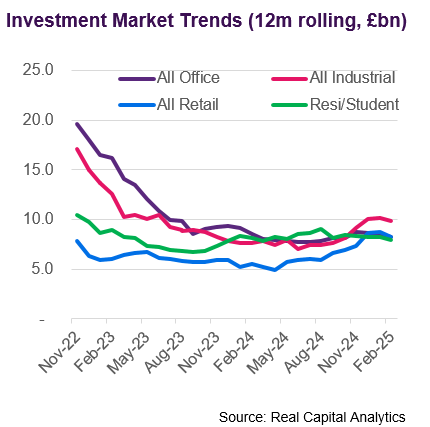

Investment market activity

Preliminary data from Real Capital Analytics indicate that just £1.3bn of transactions completed in February, a weak number even by recent standards, and only half the volume recorded in January. Minimal levels of activity were consistent across all sectors in February.

The largest deal in February, the only one to exceed £100m, was a £116m forward funding by Goodstone Living of 360 BTR flats in Dagenham. The scheme is part of the first phase of the regeneration of the former Ford stamping plant site, a JV between Peabody and the Hill Group.

The only significant logistics deal reported to have closed in February was the acquisition of the Sainsburys distribution centre in Haydock by Tritax Big Box REIT for £75m. According to RCA, the 625,000 sq ft asset traded at a 6.0% yield and a value of £120 / sq ft. Vendor Mutual Finance acquired the asset via a sale and leaseback in 1997.

Another significant deal involving a supermarket was the buyback by Tesco of their 68,000 sq ft Extra store in Newmarket. The purchase price of £63m reflects a keen initial yield of circa 4.5%, and represents a 7.4% premium to the asset’s Jun ’24 valuation. The willingness of operators to agree such strong pricing to retain control of stores represents a solid underwrite to prime asset values in the sector.

Retail Parks remain a relatively active part of the market, with food elements particularly attractive to investors. Stane Retail Park in Colchester, with an Aldi and M&S Foodhall sold for £34m, whilst Eastern Avenue Retail Park in Havering, with Burger King and Costa Coffee sold for £26.8m (5.5%). Elsewhere, Orchard Street acquired St Georges Retail Park, Leicester, from Tritax Big Box REIT for an undisclosed sum. |

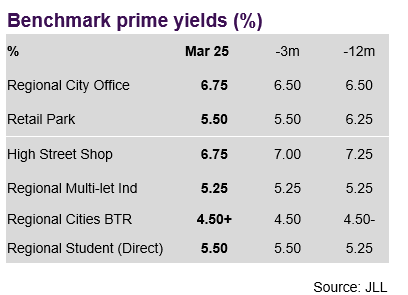

Market yields

Gilt yields remain volatile against a background of rapidly evolving global concerns. At the time of writing the ten-year Gilt yield was at 4.6%, down from a January peak close to 5%, but markedly higher than the circa 4% seen at this time last year. More encouragingly, the five-year swap rate has dipped back below 4%, in line with its level 12 months ago.

A stagnating economy and fears over the impact of rising employment costs have taken some of the momentum away from the emerging recovery in retail values. JLL had been primed for benchmark yields to firm up further for Retail Parks, Prime Shops and Dominant Shopping centres, but they now expect them to stay flat in the short-term.

Even flat yields would be a relief for the regional office market. JLL perceive that benchmark prime yields have softened by a further 25bp in top regional cities and sub-regional cities, to 6.75% and 8.75% respectively. Their only spot of optimism for offices is for the mid-sized (£40m-£125m) City of London benchmark, which they expect to come in from its current level at 5.5%.

A combination of higher Gilt yields and slowing rental growth seems to have caused some softening of BTR values. JLL estimate that benchmarks for Prime London and Outer London have moved out by 25bp to 4.25% and 4.5% respectively. They also perceive that the prime regional benchmark is probably now a little over its previous level of 4.5%. Nonetheless, BTR appears to have been significantly more resilient than commercial sectors. |

Auctions

Allsop’s auction rooms reflected the quiet start to the year. The February and March sales combined raised just over £77m, well down on the total of almost £115m raised in the same auctions last year (even if sales post auction could still increase this year’s figure).

The trend for larger lots continued, with 25 lots listed at guide prices of £1m or more. However, of these only four ended up being sold in the room. Whilst three went unsold on the day, it is not clear how many of the others achieved sales prior to the auction. The highest value lot, a Royal Mail sorting office in Livingstone with a guide price of £7.8m, was withdrawn prior to the auction.. |

Market forecasts

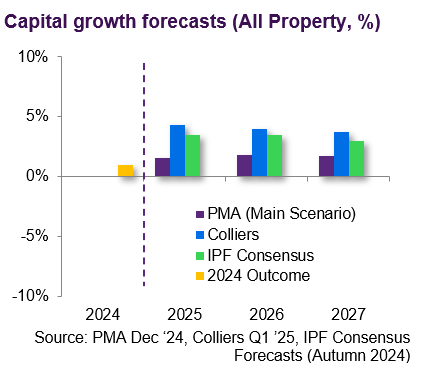

Real Estate advisory Colliers have slightly tempered their optimism for short-term capital growth, but nonetheless anticipate that average values will be almost 15% higher at the end of 2027 than they were at the start of this year. A previous prediction of 6.2% capital growth this year was at the more bullish end of the market, but their new forecast of 4.2% is closer to consensus.

Colliers’ prediction of solid capital growth of circa 4% per annum over the three-year horizon is underwritten by their expectation of steady rental growth (circa 2.7% per annum). Their forecast also assumes a small amount of yield compression to reflect a gradual easing of the interest rate environment.

Colliers expect the delta between sectors to be far smaller than in recent years, but still anticipate outperformance for the Industrial sector. They predict 3-year capital growth of c4% per annum for Industrial, which they expect to be almost entirely underwritten by 3.75% p.a. rental growth.

They expect a solid if unspectacular recovery for offices, with 3.6% p.a. capital growth from a combination of rental growth and yield compression. Retail is expected to lag slightly behind but still deliver capital growth of c3% p.a., supported by rental value growth of c2.2% p.a. |

Looking forward

An optimistic take on the current situation would be that the chaos of the early Trump era will either settle down, or that investors will simply start to get used to it and turn their focus back to things that they can control. There do at least seem to be encouraging noises regarding the deal pipeline, with a good range of sizeable office and retail assets reported to be under-offer or heading that way. The commitment by Norges, the giant Norwegian sovereign wealth fund, of over half a billion pounds for a 25% stake in Shaftesbury’s Covent Garden estate is a solid vote of confidence in the UK market. Elsewhere, it is not likely to take much for investors to rekindle their enthusiasm for beds and sheds which has dominated the investment market in recent years.

Whilst Gilts have been buffeted by geopolitical turbulence, swap rates do at least offer some encouragement with regards to interest rates. Whilst Gilt yields remain some way above where they were 12 months ago, swap rates have settled back down, with the five-year SONIA swap priced at just under 4% at the time of writing. This indicates market confidence that the path of base rate remains firmly downwards. |

Visit us

Discover a wealth of

real estate expertise, regardless of your business level or stage.

|

| If Gilt yields were to stabilise at their currently relatively elevated levels, required returns for property investment would start at around 6.5%. This does not seem too much of a stretch for a market where prime yields range from 4% to 6% for residential, industrial and Central London offices, sectors which have been delivering consistently robust rental growth over the last couple of years. Elsewhere, prime yields for retail and regional offices range from 5.5% to 9%, a starting point that requires little or no income growth to deliver an acceptable return. If geopolitics were to return to merely normal levels of anxiety and uncertainty, and Gilt yields respond accordingly, real estate investment might even start to look rather cheap. |

|

|

If you would like to opt out, please get in touch with your Relationship Manager.

The Royal Bank of Scotland plc, The Royal Bank of Scotland N.V, or an affiliated entity (‘RBS’) and for the purposes of Directive 2004/39/EC has not been prepared in accordance with the legal and regulatory requirements to promote the independence of research. Regulatory restrictions on RBS dealing in any financial instruments mentioned at any time before this document is distributed to you do not apply. This document has been prepared for information purposes only. It shall not be construed as, and does not form part of an offer, nor invitation to offer, nor a solicitation or recommendation to enter into any transaction or an offer to sell or a solicitation to buy any security or other financial instrument. No representation, warranty or assurance of any kind, express or implied, is made as to the accuracy or completeness of the information contained herein and RBS and each of their respective affiliates disclaim all liability for any use you or any other party may make of the contents of this document. The contents of this document are subject to change without notice and RBS does not accept any obligation to any recipient to update or correct any such information. Views expressed herein are not intended to be and should not be viewed as advice or as a recommendation. RBS makes no representation and gives no advice in respect of any tax, legal or accounting matters in any applicable jurisdiction. This document is not intended for distribution to, or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. The information contained herein is proprietary to RBS and is being provided to selected recipients and may not be given (in whole or in part) or otherwise distributed to any other third party without the prior written consent of RBS. RBS and its respective affiliates, connected companies, employees or clients may have an interest in financial instruments of the type described in this document and/or in related financial instruments. Such interest may include dealing in, trading, holding or acting as market-makers in such instruments and may include providing banking, credit and other financial services to any company or issuer of securities or financial instruments referred to herein. The Royal Bank of Scotland plc. Registered in Scotland No. 90312. Registered Office: 36 St Andrew Square, Edinburgh EH2 2YB. The Royal Bank of Scotland plc is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and Prudential Regulation Authority. The Royal Bank of Scotland N.V., established in Amsterdam, The Netherlands. Registered with the Chamber of Commerce in The Netherlands, No. 33002587. Authorised by De Nederlandsche Bank N.V. and regulated by the Authority for the Financial Markets in The Netherlands. Agency agreements exist between different members of The Royal Bank of Scotland Group plc.

© Copyright 2024 The Royal Bank of Scotland plc. All rights, save as expressly granted, are reserved. This communication is for the use of intended recipients only and the contents may not be reproduced, redistributed, or copied in whole or in part for any purpose without The Royal Bank of Scotland plc’s prior express consent.

|

|

|