If you cannot see the graphic or access the links within this message please go to the source

|

|

|

Bond volatility leaves stirring property market slightly shaken

| There seemed to be a sense of growing optimism around the commercial property sector as 2024 drew to a close. Much of this was down to the belief that a steady downward trend in interest rates through 2025 would underwrite a gradual recovery in asset values. However, just a few days into the New Year this fragile confidence was tested by a surge in Gilt yields and accompanying rise in medium-term interest rates. Whilst short-term gyrations in government bond yields have no measurable impact on direct property values, they certainly won’t have helped sentiment at a time when many investors are gearing themselves up to re-enter the market.

This was reflected in REIT prices, with the FTSE 350 REITs index giving up around 5% over the first two weeks of the year. However, REITS are more correlated with the wider equity market than with direct real estate values, and the FTSE 250 recorded a similar decline over the same period. The most direct effect of higher Gilt yields on real estate pricing is likely to be on the most bond-like income streams, which will appear less valuable today than they did a couple of months ago. However, broader implications for real estate will depend on the underlying root causes of those higher Gilt yields. |

Many have rushed to blame the Chancellor, drawing parallels with the spike in Gilt yields following the Truss / Kwarteng “mini budget” in 2022. It’s certainly true that the Autumn budget has done little to improve business sentiment and the desire to invest for growth. However, the timing of the spike doesn’t fully support the case for the prosecution, and it seems likely that concerns over the impact of the incoming Trump administration and changing mood music from the Fed had at least as much impact. In the UK, markets went from anticipating 3 or 4 cuts to base rate in 2025, to expecting only one or two.

Nonetheless, the impact on medium-term interest rate swaps has not been as dramatic as movements in the Gilt market. When it comes to comparisons against bonds, the “real” in real estate presents a crucial advantage. Commercial property may not be a genuine inflation hedge in the long-term, but it has been delivering some mitigation recently. Rental value growth has been positive across most sub-sectors over the last year and is expected to remain so despite the tepid economy. |

|

Commercial property returns

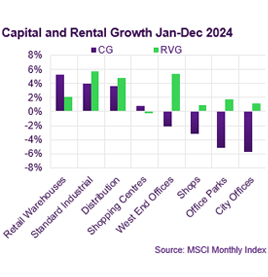

According to MSCI, average commercial property values increased by 0.6% in December, and by 1.3% in the Q4. Capital values are now 1.1% higher than they were at the start of 2024, even if they remain an average of 23.6% below their June 2022 highwater mark.

Retail Warehouses were the strongest performing sub-sector in 2024, delivering average value growth of 5.2%. Shopping Centres managed to eke out positive growth for the year (+0.8%) for the first time since 2015. Shops continued to struggle, with values down by 3.2% year-on-year.

The recovery in Industrial values has started to pick up pace, growing by 2.3% in the final Quarter of 2024, taking annual growth to 3.9%. This recovery has been supported by robust rental growth of 5.5%, only down marginally from the previous year (7.5%). Despite this strong rental performance, capital values remain almost 24% below their 2022 peak.

Offices were the clear underperformer, with capital values down by 5.7% year-on-year. This came despite rental values growing by an average of 2.1% across the sector. London West End was the most resilient sub-market, with asset values down by just 2.1%, as rents rose by 5.4%. In contrast, office values in Scotland were down almost 18% on average. |

|

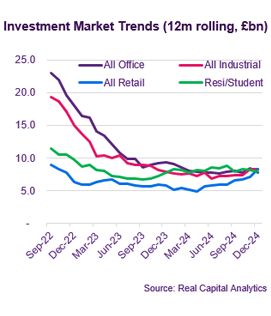

Investment market activity

Preliminary data from Real Capital Analytics show a relatively strong end to 2024, at least by the very weak standards of recent years. £3.6bn traded in December, taking the Q4 total to £11.4bn. This compares to £9.6bn in Q4 ’23 and just £7.4bn in the final quarter of 2022. The full-year total is currently estimated at £42.8bn up by 15% on the previous year.

The largest deals in December were dominated by the Retail sector – not something that has happened too often over the last decade. Indeed, Retail was not far off from being the most invested sector in Q4, with £2.6bn of deals leaving it only marginally behind offices (£2.8bn).

The largest single-asset deal of the month was the acquisition by LandSec of the Liverpool One shopping centre from a JV between ADIA and Grosvenor for £533m. The sale price represents a yield of 6.9%, one of the keenest yields seen in the shopping centre sector in recent years. Elsewhere, New River acquired the Capital & Regional portfolio of six centres for £147m as part of their acquisition of the wider business.

Retail Parks were persistently one of the most in demand sub-sectors in 2024, and the year was capped ff by the sale of 16 parks by Oxford Properties to Redevco. for £518m. The price was estimated by Green Street to reflect a yield of 5.5-6.0%.

December saw the completion of one of the largest single asset West End office deals in recent years, with the sale of 11-12 St James’s Square for £162m. The vendor, Chinese Estates had been looking for offers around £200m. Nonetheless, the achieved price reflects the relative resilience of prime West End assets, being only slightly less than the price they paid in 2017, despite now being almost entirely vacant.

|

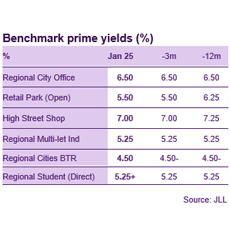

Market yields

Sticky inflation, the fallout from the Autumn budget and concern about the impact of Donald Trump’s policies, have combined to drive up Gilt yields. From a low of around 3.75% in mid-September, the ten-year Gilt yield has got close to 5% in January. Swap rates have also been impacted with 5-year Sonia swaps up by 40bp within the last month, to 4.25%.

This upward trend in medium-term interest rates, pricing in just one or two cuts to base rate this year, have perhaps moderated the compression in property yields seen in mid-2024. JLL consider most benchmarks to be stable at their current level, but still see further weakness for the largest City office assets. The current benchmark for City assets above £125m is assessed to be 5.75%, but transactional evidence has been very limited.

Despite adverse interest rate movements, JLL do see some prospects for yield compression, including for Industrial assets, retail parks and dominant shopping centres. For the last of these, JLL assess that the prime benchmark for came in by 25bp to 7.5%. The key evidence for this was the sale of Liverpool One, where the initial yield was reported to be just under 7%.

In contrast, JLL estimate that benchmarks for student accommodation have softened over the last month. Benchmarks for Prime London and Inner London have moved out by 25bp to 4.5% and 4.75% respectively, whilst Super Prime and Prime regional are deemed to have softened slightly from their December levels of 5.0% and 5.25% respectively. |

Auctions

Allsop report that they raised £35m from sales in their final auction of the year in December. They announced total sales for the year of £456m from the sale of 576 lots. This reflects an overall success rate of 88%, which includes sales agreed before and after the auction, as well as those closed in the room. The average sale price in 2024 was £790k, up from £685k in 2023.

The highest price achieved in December was for a vacant office block in Mayfair which sold for over £5.5m. The Grade II listed building on Grosvenor Street sold for around £1,000 per square foot. Industrial assets, long income and retail with residential uppers continued to attract strong interest. |

Market forecasts

Despite being one of the more cautious voices in the market, independent forecasters PMA’s main scenario predicts a steady (if slow) recovery from here on in. They expect average capital values across the mainstream commercial sectors to rise by just over 5% over the next 3 years.

PMA expect that multi-let Industrial to outperform other traditional sectors over the next 3 years, with cumulative growth of around 13%. Distribution warehouses will follow slightly behind with cumulative growth of 7%. Returns in both sectors are expected to be driven by rental growth.

PMA are notably more bearish for Retail, with very little in the way of cyclical recovery expected for much of the sector. Central London retail is the notable exception with 3-year growth of circa 10% predicted. Retail parks and shopping centres are only expected to eke out marginal capital growth over three years, even though rental growth is expected to broadly match inflation.

PMA anticipate that Central London offices will deliver moderate capital growth of c5% over 3 years, the Big 6 Cities will be flat, provincial markets will fall 5% and the M25 West will decline by 10%. Steady rental growth is expected in most regions, but this is expected to be undermined by depreciation.

|

|

Looking forward

Of course, if the backdrop of elevated Gilt yields persists, it will undoubtedly have an impact on institutional investors’ appetite for real estate. If a pension fund can get a 5% return guaranteed from the UK government, they are going to be looking for a return of at least 7-8% from direct real estate to compensate for illiquidity and obsolescence, tenant risk, and higher required levels of management oversight. According to independent forecasters PMA, total returns at such a level should be achievable, at least in the stronger performing “beds and sheds” sectors, but are perhaps unlikely to be delivered without taking a level of leasing or development risk that many institutions may be uncomfortable with.

The outlook for the real estate market seems to be to expect broad-based market rental growth, perhaps matching or even exceeding broader inflation, but that prospects for cyclical market-wide yield compression are limited.

|

Visit us

Discover a wealth of

real estate expertise, regardless of your business level or stage.

|

| Market beta therefore is likely to be an income return, garnished by a moderate rental growth, perhaps delivering around 5-7% after depreciation. Unlocking the alpha to deliver returns of 8%+ will require active asset management and the judicious application of capital expenditure. Unusually therefore we might end up with a market where, rather than core assets leading the recovery, investor activity will focus on value-add opportunities which can best target the parts of the market where current supply is lagging occupier demand. Such opportunities could come from the retail and office sectors which have largely been deserted by Core investors in recent years. Investors taking the plunge in these sectors will hope to buy cheap and reposition, delivering a core product just in time for institutional investors to return to the market as the cyclical recovery progresses. |

|

|

If you would like to opt out, please get in touch with your Relationship Manager.

This document has been prepared by National Westminster Bank Plc or an affiliated entity (“NatWest”) exclusively for internal consideration by the recipient (the “Recipient” or “you”) for information purposes only. This document is incomplete without reference to, and should be viewed solely in conjunction with, any oral briefing provided by NatWest. NatWest and its affiliates, connected companies, employees or clients may have an interest in financial instruments of the type described in this document and/or in related financial instruments. Such interests may include dealing in, trading, holding or acting as market-maker in such instruments and may include providing banking, credit and other financial services to any company or issuer of securities or financial instruments referred to herein. NatWest is not and shall not be obliged to update or correct any information contained in this document. This document is provided for discussion purposes only and its content should not be treated as advice of any kind. This document does not constitute an offer or invitation to enter into any engagement or transaction or an offer or invitation for the sale, purchase, exchange or transfer of any securities or a recommendation to enter into any transaction, and is not intended to form the basis of any investment decision. This material does not take into account the particular investment objectives, financial conditions, or needs of individual clients. NatWest will not act and has not acted as your legal, tax, regulatory, accounting or investment adviser; nor does NatWest owe any fiduciary duties to you in connection with this, and/or any related transaction and no reliance may be placed on NatWest for investment advice or recommendations of any sort. Neither this document nor our analyses are, nor purport to be, appraisals or valuations of the assets, securities or business(es) of the Recipient or any transaction counterparty. NatWest makes no representation, warranty, undertaking or assurance of any kind (express or implied) with respect to the adequacy, accuracy, completeness or reasonableness of this document, and disclaims all liability for any use you, your affiliates, connected companies, employees, or your advisers make of it. Any views expressed in this document (including statements or forecasts) constitute the judgment of NatWest as of the date given and are subject to change without notice. NatWest does not undertake to update this document or determine the accuracy or reasonableness of information or assumptions contained herein. NatWest accepts no liability whatsoever for any direct, indirect or consequential losses (in contract, tort or otherwise) arising from the use of this material or reliance on the information contained herein. However, this shall not restrict, exclude or limit any duty or liability to any person under any applicable laws or regulations of any jurisdiction which may not be lawfully disclaimed. The information in this document is confidential and proprietary to NatWest and is intended for use only by you and should not be reproduced, distributed or disclosed (in whole or in part) to any other person without our prior written consent.

National Westminster Bank Plc. Registered in England & Wales No. 929027. Registered Office: 250 Bishopsgate, London EC2M 4AA. National Westminster Bank Plc is authorised by the Prudential Regulation Authority, and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

|

|

|